News

Boeing and Carbonfuture Sign Multi-Year Agreement for at least 40,000 Tonnes of Durable Carbon Removal

Boeing and Carbonfuture Sign Multi-Year Agreement for at least 40,000 Tonnes of Durable Carbon Removal

Learn More

This article was originally published by the Word Economic Forum. The original version is available here.

1. Carbon dioxide removal is critical to achieving net zero, yet current volumes remain far below the science-required levels because the financial architecture is not fit for purpose.

2. Scaling carbon dioxide removal requires a financial architecture that makes projects bankable, aligns risk with the right capital types and enables capital to move with confidence.

3. The key barrier is the 'missing middle': projects that are beyond early equity, but not yet bankable, are too risky for lenders and too capital-intensive for venture investors, creating a capital gap that blocks scale.

Carbon dioxide removal will only scale when the financial architecture evolves to make it bankable.

Carbon dioxide removal is critical to achieving net zero. The University of Oxford's 2024 State of Carbon Dioxide Removal Report estimates that the world must remove 7–9 billion tonnes of CO2 annually by 2050 to stay within a 1.5°C pathway. Today, only ~2 million tonnes of durable carbon removals are verified each year, which is less than 0.1% of what is needed.

The technologies exist. What’s missing is the financial architecture that can price and appropriately allocate risk, deliver liquidity and finance infrastructure at scale.

Only $836 million of equity capital was invested into durable carbon dioxide removal companies in 2024, according to Carbon Dioxide Removal.fyi’s 2024 Market Report. The State of Durable Carbon Dioxide Removal Financing Report shows 70% of suppliers expect to raise capital within six months and 43% within three months, underscoring the near-term liquidity pressure facing the sector. The European Commission estimates that meeting Europe’s near-term climate targets will require €2.4–6.7 billion in cumulative carbon dioxide removal investment by 2030.

Without a functioning capital stack, projects wait for funding and investors wait for bankable assets.

Misaligned expectations: The conversation has focused too narrowly on 'demand signals' or on why venture capital and banks should do more. Both are necessary, but insufficient. Venture investors are designed for high-return, high-risk innovation, not capital-intensive infrastructure. On the other hand, banks will not finance unproven projects that lack cash flow visibility.

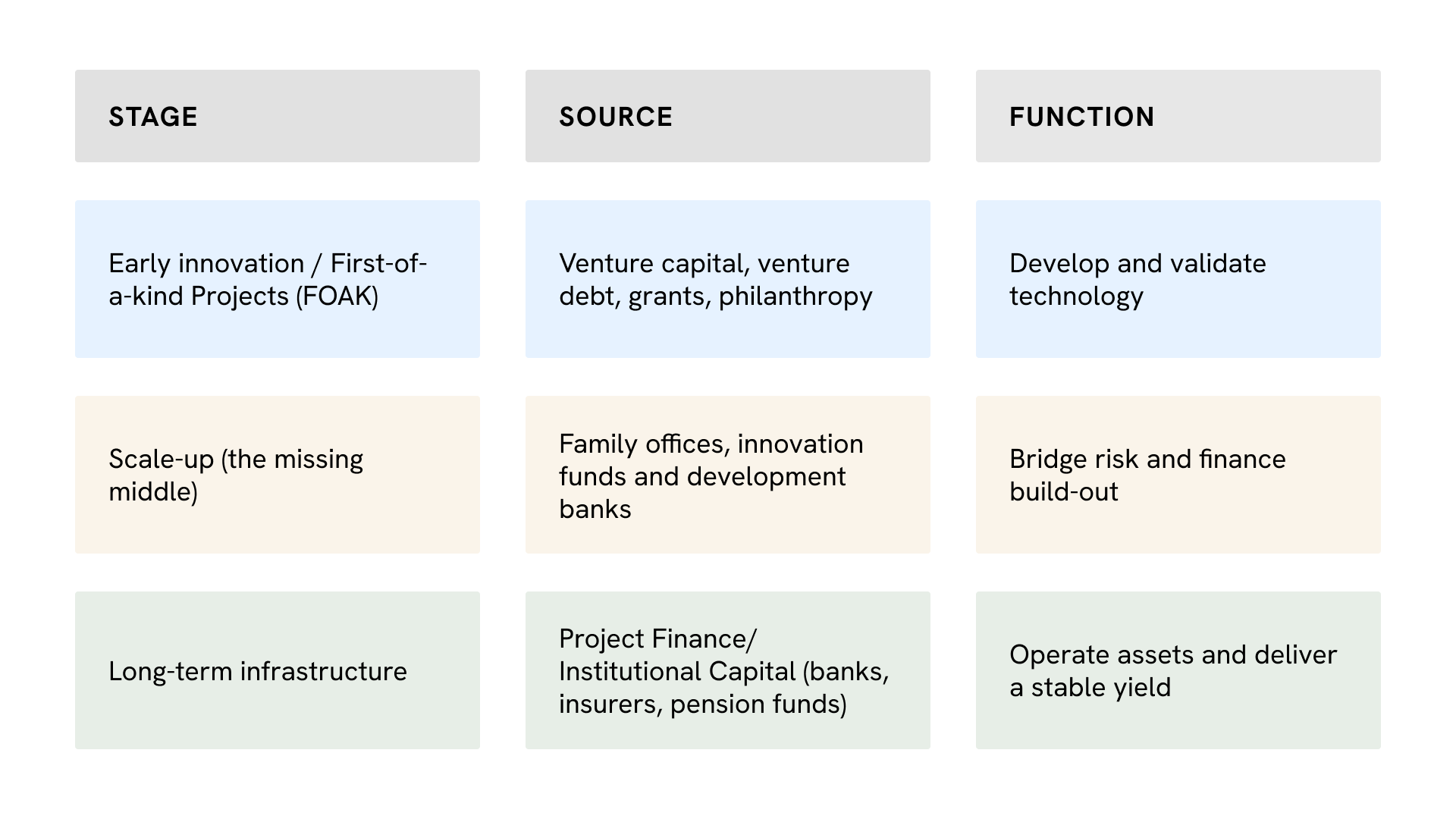

The missing middle: Projects that are beyond early equity, but not yet bankable, are too risky for lenders and too capital-intensive for venture investors. Barclays’ 2024 Climate Tech Report estimates that only about 16% of global climate-finance needs are being met, leaving a vast 'missing middle' where catalytic or blended finance is required to get climate technologies to scale. Only a fraction of carbon dioxide removal projects currently access this type of transitional capital.

The State of Durable Carbon dioxide removal Financing Report confirms a near-absence of $1–5 million investors who can bridge the gap between grants and institutional capital. This 'missing middle' is where risk-tolerant capital from family offices, development banks, sovereign wealth and public-financed innovation funds and impact funds must operate.

Structural mismatches: Carbon dioxide removal suppliers and financiers still speak different financial languages. To suppliers, 'project finance' means early, non-dilutive capital for technology deployment. To banks and other institutional investors, it means long-term, de-risked assets with contracted cash flows backed by blue-chip counterparties. Even 'bankable offtakes' often fail standard tests: e.g. contracts may allow termination within 18 months, yet issuance delays often exceed that, making them unsuitable as collateral.

Long and costly transaction cycles: These amplify the underlying constraints as most lenders cannot offer the long tenors many projects require, private capital seeks 15%+ returns even with strong offtakes and reputational and certainty requirements remain high. Together, these factors slow capital deployment despite growing demand.

These inefficiencies prevent capital from finding, trusting and deploying into credible assets.

Scaling carbon removal requires a financial architecture that makes projects bankable, aligns risk with capital type and uses trusted data and other appropriate risk-mitigating levers to enable credit risk assessment and performance-linked yields.

Predictable demand is the base of any investable market. Corporate buyers, such as Microsoft and buyer clubs (Frontier, NextGen CDR), have committed over $10 billion to advance durable carbon removal through long-term offtakes, according to CDR.fyi.

Governments are beginning to establish the policy backbone for bankable carbon removal. The UK has introduced Contracts for Difference (CfDs) for carbon capture and removal — creating stable price floors that unlock private finance — and is moving to integrate engineered removals into the UK Emissions Trading Scheme. Canada now provides an Investment Tax Credit covering up to 60% of CAPEX for carbon removal technologies, while in the US, the 45Q tax credit continues to be one of the strongest drivers of early project economics.

Reliable, multi-year demand gives suppliers the economic basis to scale and provides project investors and lenders with predictable cash flows they can underwrite with confidence. Creditworthy, 'investor-grade' buyers further strengthen project bankability and can materially lower the cost of capital.

Capital must move through a structured stack where each layer matches its risk tolerance, cost of capital and expected return.

In practice, this stack also reflects the seniority of losses: early equity absorbs first risk, subordinated or blended finance bridges the transition and project equity and debt provides the lowest-cost capital once cash flows are predictable.

Independent monitoring, reporting and verification and due diligence services turn project performance — from project development through to carbon storage — into measurable, auditable results. This transparency across the full project lifecycle reduces credit risk and allows lenders to link disbursements to verified milestones.

This model finances infrastructure before the first tonne is removed, demonstrating how grants, bonds and buyer commitments can align to make carbon removal bankable.

The carbon removal sector mirrors renewables in the late 2000s. Once feed-in tariffs, project finance and data verification aligned, renewable investment grew from $33 billion (2004) to $728 billion (2024).

Carbon removal can follow the same trajectory — if the financial architecture evolves to price risk accurately, create liquidity and channel capital efficiently.

Carbon removal will scale to science-required levels only through a functioning financial architecture that moves capital with confidence. The time to build that system is now.

If your organization — whether a corporate buyer, financial institution or development partner — is interested in helping build this financial architecture for carbon removal, please contact the authors to explore collaboration opportunities.

The authors thank the following reviewers for their thoughtful and constructive contributions to this article: Kash Burchett (HSBC), Cindy Jia (ING), Lucas Joppa (Haveli Investment), Henry Waite (Kumo) and Max Zeller (Carbon Removal Partners). All views expressed in this article are solely those of the authors and do not represent the positions, opinions, or endorsements of the reviewers or their respective organizations.

At Carbonfuture, we build trust throughout the carbon removal journey with our rigorous, data-driven approach, ensuring unmatched quality and reliability of carbon removal.